Budget 2020 for NRIs in the GCC

The Finance Bill 2020 has been passed in the Lok Sabha on 23 March 2020 with certain modifications and is currently awaiting the Presidential assent. The Budget has proposed certain amendments in the residency related provisions in the IT Act , which have been untouched for many years. The purpose of this document is to analyze the impact of these amendments to an NRI, especially to one residing in a GCC country.

Residency Provisions

Each country defines the concept of residency which is of importance to determine how an individual will be chargeable to tax in its jurisdiction. In India, charge of income tax is not based on domicile or citizenship. The Indian tax liability depends on the residential status of an individual based on his physical stay in India.

For tax purposes, the residential status of an individual is classified as Ordinarily Resident (‘OR’), Not Ordinarily Resident (‘NOR’) or Non-Resident (‘NR’), based on the number of days of his physical stay in India in a Financial Year (‘FY’).

In principle, an OR taxpayer is subject to tax on his worldwide income whereas a NR is only taxed on Indian sourced income. NOR is taxed on the Indian sourced income like a NR and also taxed for income from abroad if it is from a business controlled or profession setup in India.

Current Residency Conditions

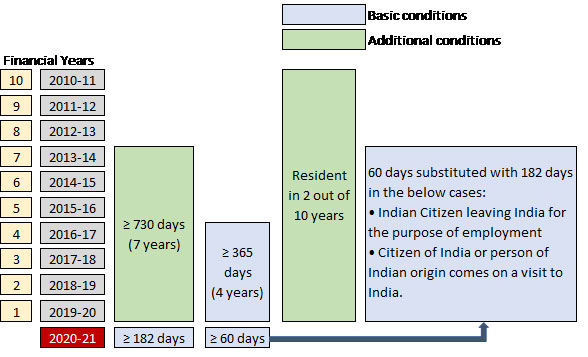

In order to determine residential status in India, the conditions to be satisfied can be classified as:

| A. | Basic Conditions: |

| (i) | Stay in India in the FY for a period of 182 days or more; OR |

| (ii) | Stay in India for a period of 60 days or more during the FY and 365 days or more during the 4 years preceding the relevant FY.

The period of 60 days can be extended to 182 days in following circumstances:

(a) Citizen of India, who leaves India in any previous year for the purpose of employment outside India;

(b) Citizen of India or a Person of Indian Origin (PIO) who being outside India, comes on a ‘visit’ to India in any FY.

|

| B. | Additional Conditions: |

| (i) | He/she has been non-resident in India in 9 out of 10 fiscal years preceding the relevant FY; OR |

| (ii) | He/she has been in India for a period of less than 730 days during 7 years preceding the relevant FY. |

Table 1: Existing Residency Provisions

The manner of satisfaction of the above conditions for determining the residential status has been tabulated below:

| Residential Status | Basic Condition | Additional Conditions |

| OR | At least one | None |

| NOR | At least one | At least one |

| NR | None | Not Applicable |

A pictorial representation of the current residency provisions have been provided below:

Amendments Proposed in Budget 2020

? Period of 182 days referred to under Basic Condition A(ii)(b) for a citizen of India or a PIO who being outside India, comes on a ‘visit’ to India in any financial year has been reduced to 120 days in case of citizen of India or Person of Indian Origin having total income (other than income from foreign sources) exceeding Rs 15 lakhs during the previous year;

? New “Deemed Resident” concept (Refer condition A(iii) under Table 2)

? Two new Additional Conditions have been inserted (Refer conditions B(iii) and B(iv) under Table 2: Amended Residency Provisions)

The residency conditions as it stands after the amendment have been tabulated below:

| A. | Basic Conditions: |

| (i) | Stay in India in the FY for a period of 182 days or more; OR |

| (ii) |

Stay in India for a period of 60 days or more during the FY and 365 days or more during the 4 years preceding the relevant FY.

The period of 60 days can be extended in the following circumstances:

(a) In case of Citizen of India, who leaves India in any previous year for the purpose of employment outside India – extended to 182 days;

(b) In case of Citizen of India or a PIO who being outside India, comes on a ‘visit’ to India in any FY:

(1) Having total income (other than income from foreign sources) not exceeding Rs 15 lakhs during the previous year – extended to 182 days

(2) Having total income (other than income from foreign sources) exceeding Rs 15 lakhs during the previous year – extended to 120 days |

| (iii) | An individual being a citizen of India, having total income (other than the income from foreign sources) exceeding Rs 15 lakhs during the previous year shall be deemed to be resident in India in that previous year, if he is not liable to tax in any other country or territory by reason of his domicile or residence or any other criteria of similar nature (“Deemed Resident”) |

| B. | Additional Conditions: |

| (i) | He/she has been non-resident in India in 9 out of 10 fiscal years preceding the relevant FY; OR |

| (ii) | He/she has been in India for a period of less than 730 days during 7 years preceding the relevant FY; OR |

| (iii) | In respect of persons referred to in Condition A(ii)(b)(2), who has been in India for a period of 120 days or more but less than 182 days; OR |

| (iv) | Citizen of India deemed as resident under Condition A(iii). |

Table 2: Amended Residency Provisions

[Texts highlighted in green are where amendments have been made]

New “Deemed Resident” Concept

Another significant amendment with regard to the residency condition that created an unrest among various NRIs, especially in the GCC region, is the new “Deemed Resident” provisions.

The Memorandum to the Finance Bill, 2020 raised the concern of “stateless persons” or in other words, country-less persons. The relevant extract of the Memorandum has been provided below:

“The issue of stateless persons has been bothering the tax world for quite some time. It is entirely possible for an individual to arrange his affairs in such a fashion that he is not liable to tax in any country or jurisdiction during a year. This arrangement is typically employed by high net worth individuals (HNWI) to avoid paying taxes to any country/ jurisdiction on income they earn. Tax laws should not encourage a situation where a person is not liable to tax in any country.”

Though the Finance Bill, as drafted initially, created various confusion, the amended Finance Bill has classified Indian citizens having total income, other than income from foreign sources, exceeding Rs 15 lakhs during the previous year as HNWI.

"Income from foreign sources" means income which accrues or arises outside India (except income derived from a business controlled in or a profession set up in India).

A person who qualifies as a deemed resident would automatically be given the status of NOR, thereby, bringing to tax in India his foreign income from business controlled or profession set up in India also.

Taxability of NOR

It is interesting to note that NOR status is unique to India and that no other country has such an intermediate residential status. Some countries provide exemption to foreign source income to their residents. For example, Singapore follows territorial basis of taxation whereby income earned abroad by a person resident in Singapore is not taxed in Singapore unless the same is received in Singapore.

As compared to an NR, NOR is additionally chargeable to tax in India in respect of their income accruing outside India from a business controlled from India or from a profession set up in India. The expression 'business controlled in India' means that the 'head and brain' of the business - the controlling power - should be situated in India and should direct the business activities from India. Thus, foreign passive incomes like interest, dividend, royalty etc. would not be taxable in India for a person who is NOR. Even share of profit of a partnership firm or any other business income would not be taxable in India, if the business in respect of which such income arises is not controlled from India. If business is controlled from India, then the income is taxable in India. In other words, all foreign sourced income of a NOR is normally not taxable in India unless it is derived from a business controlled in or a profession set up in India.

Impact of “Deemed Resident” Provisions on NRIs in the GCC Countries

The “deemed resident” provisions could have significant impact on the NRIs in the GCC as individuals are not subject to income tax in the GCC countries. The impact arises from the interpretation of the term “liable to tax” used in the proposed deemed resident provisions.

The Supreme Court in the case of Azadi Bachao Andolan distinguished between “liable to tax” and “subject to tax”. The Court observed that liability to taxation is a legal situation whereas payment of tax is a fiscal fact. For the purpose of determination of residence, what is relevant is the legal situation, namely, liability to taxation, and not the fiscal fact of actual payment of tax. In other words, irrespective of whether or not the GCC Government levies taxes on individuals, once the right to tax GCC residents vests only with the GCC Countries, that right, whether exercised or not, continues to remain exclusive right of the GCC Countries . In such a context, NRIs in the GCC can take a view that deemed resident provisions would not apply to them. However, considering the ambiguity in the provision, it is recommendable for any tax resident NRIs from any of the GCC countries to obtain an advance ruling to get more clarity on this aspect.

However, in order to prove residency in the other country, an NRI would be required to provide a Tax Residency Certificate (TRC) from the competent authority of the other country in which the person is a resident. At present, there are some practical difficulties in obtaining a TRC from the GCC Countries.

Tax Residence in the GCC

Given below are the residency conditions in the tax treaties entered by India with the GCC countries:

| Country | Residency Condition |

| Bahrain | No tax treaty with India |

| UAE | Individual present in UAE for at least 183 days in the calendar year |

| Kuwait | Indian national present in Kuwait for at least 183 days in the fiscal year |

Oman

Qatar

Saudi Arabia | Resident of a contracting state means a person who, under the laws of that Contracting State, is liable to tax therein by reason of his domicile, residence, place of management or any other criterion of a similar nature. |

India has not entered into a tax treaty with Bahrain. Therefore, a person residing in Bahrain, who is deemed as a resident in India under the new residency conditions, would not be able to claim any treaty benefit of residence-based taxation. However, NRIs based out in Bahrain should manage to obtain TRCs from the Ministry of Finance on a safer side to prove their tax residency in Bahrain.

Our Thoughts

The Government has made a fine attempt at clearing the ambiguities that had arisen initially. However, the deemed resident provisions tend to discriminate amongst NRIs as an NR who is resident in the GCC but are not subject to tax in that country by virtue of domestic law of that country would be conferred a different residential status.

Consider the below situation:

| | Person A | Person B |

| Country of residence | Kuwait | Singapore |

| Period of stay in India in FY 2020-21 | Less than 120 days |

| Indian income | Exceeding Rs 15 lakhs |

| Residential Status | NOR | NR |

Both persons earning the same income and visiting India for the same period is conferred different residential status based on their country of residence.

Further, such provisions may also get attracted in case of such HNWI NRIs who do not qualify as resident in any country due to bona fide reasons, such as businessmen who travel frequently on account of genuine business reasons.

Moreover, considering the difficulties in obtaining a TRC, the Government would need to reach an understanding with the Government in the GCC countries regarding issuance of TRC.

On a combined reading of all the residency provisions, it would be advisable for NRIs with Indian income exceeding Rs 15 lakhs to plan their visit to India in such a manner that their average stay in India in a year does not exceed 3 months.

Sreejith Kuniyil

Partner - CAPITAIRE Consultants LLP (India, Kuwait)

[email protected]

+91 97464 00931

Disclaimer

This publication does not constitute professional advice. The document is created for information and knowledge sharing purpose only. The information in this publication has been obtained or derived from sources believed by CAPITAIRE to be reliable but does not represent that this information is accurate or complete. Any opinions or estimates contained in this publication represent the judgment of CAPITAIRE at this time and are subject to change without notice.

Readers of this publication are advised to seek their own professional advice before taking any course of action or decision, for which they are entirely responsible, based on the contents of this publication.

CAPITAIRE neither accepts nor assumes any responsibility or liability to any reader of this publication in respect of the information contained within it or for any decision readers may take or decide not to or fail to take.

Our sharing of this documentation along with such protected images with you does not authorize you to copy, republish, frame, link to, download, transmit, modify, adapt, create derivative works based on, rent, lease, loan, sell, assign, distribute, display, perform, license, sub-license or reverse engineer the images. In addition, you should desist from employing any data mining, robots or similar data and/ or image gathering and extraction methods in connection with the document.